Considering an Annuity? There May Be a More Flexible Way to Generate Income

Patrick McNamara

Considering an Annuity? There May Be a More Flexible Way to Generate Income

Annuities have long been a popular choice for conservative investors approaching retirement. They offer predictability, insulation from market swings, and the reassurance of principal protection — especially appealing for those transitioning from accumulation to income.

Those goals are sensible. Most annuity investors aren’t trying to beat the market. They want stability, income they can count on, and fewer surprises.

Why Investors Choose Annuities

Annuities are often selected because they promise:

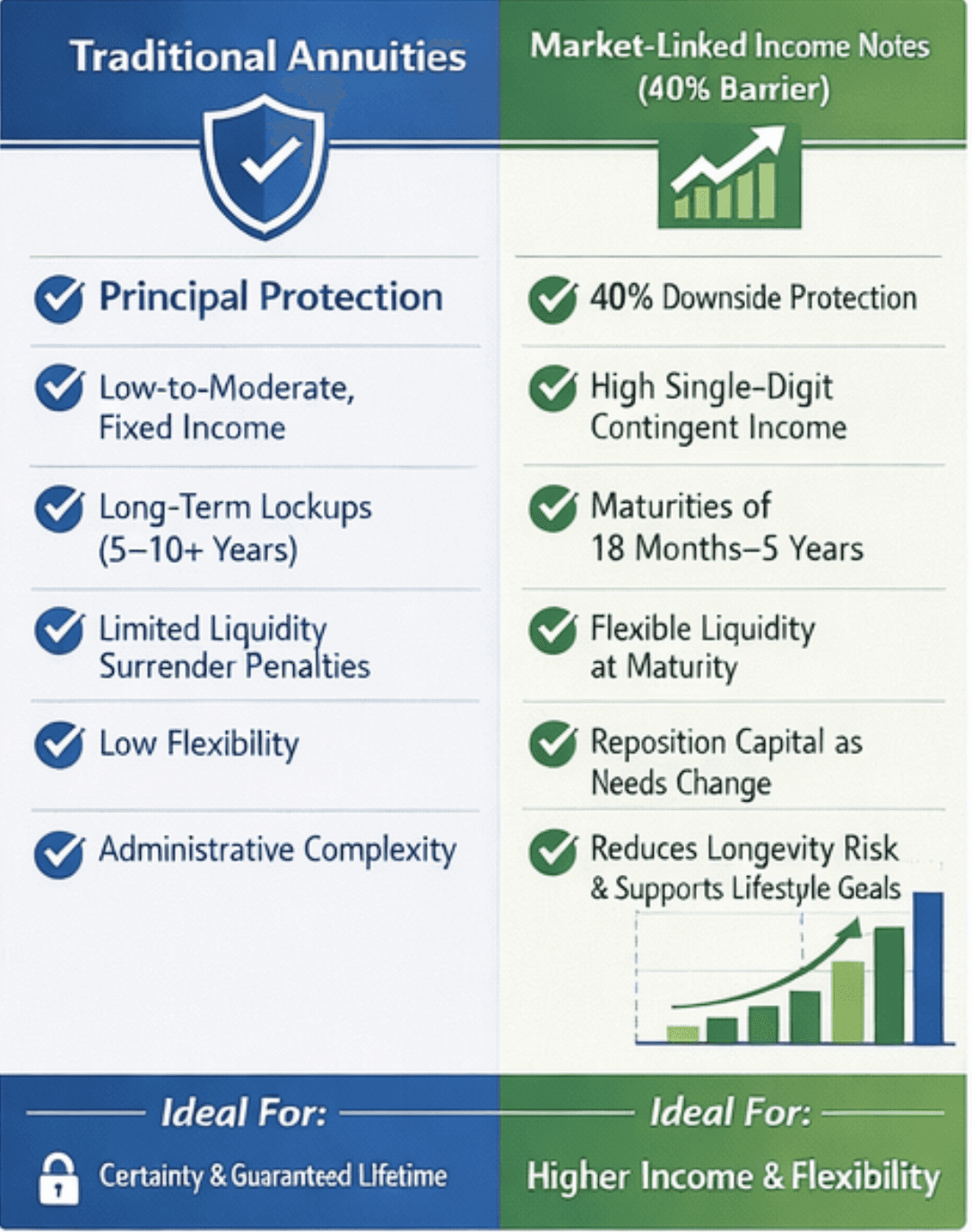

Principal protection

Predictable income streams

Reduced exposure to market volatility

A sense of long-term security

For many investors, annuities feel like a responsible, conservative solution.

The Problem: Tradeoffs That Limit Flexibility

What isn’t always clear upfront are the tradeoffs that come with that sense of safety. Over time, many annuity owners discover:

Income levels that feel modest relative to the capital committed

Limited liquidity once the contract is in place

Less flexibility as income needs or markets change

Ongoing administrative complexity

These limitations don’t make annuities “bad” — but they do explain why many conservative investors are beginning to reassess whether they’re still the best fit.

A Smarter Evolution in Retirement Income

For many investors, the question isn’t whether they want protection — it’s how that protection is structured.

Market-linked income notes are designed to support the same core goals annuity investors care about: dependable income, capital preservation, and peace of mind. In many cases, they also offer meaningfully higher income potential than traditional annuities, helping offset longevity risk by allowing retirees to draw income while keeping more of their assets working over time.

With built-in downside protection and defined maturities, these notes provide clarity around outcomes without permanently locking up capital — giving investors the ability to adapt as markets, income needs, and life circumstances change.

A Side-by-Side Look: Traditional Annuities vs. Market-Linked Income Notes

This comparison highlights why many conservative investors are reconsidering how they generate retirement income — not by taking on more risk, but by using structures better aligned with today’s realities.

Final Thought

Retirement today looks very different than it did even a generation ago. People are living longer, inflation remains a real concern, and income needs often extend far beyond what traditional planning assumptions anticipated.

In this environment, relying solely on strategies designed for shorter retirements and lower inflation can quietly increase risk — not necessarily through market volatility, but through insufficient income and the gradual erosion of purchasing power over time.

That’s why many conservative investors are beginning to think differently about how they generate retirement income. The goal isn’t to take on more risk, but to create income that can support a longer life, help offset inflation, and preserve flexibility as circumstances change. A well-structured approach can allow assets to continue working efficiently while still providing meaningful downside protection.

Sometimes the most prudent move isn’t staying with what’s familiar — it’s adapting to the realities of retirement today.

Patrick McNamara

CFP®, Financial Advisor at Claro Advisors

About the Author

Patrick McNamara, CFP® is a Financial Advisor at Claro Advisors

with nearly 30 years of experiencein the financial services industry.

He has held senior roles at Fidelity Investments, Goldman Sachs, and

Morgan Stanley. He founded StructuredNotes.com to educate investors

on institutional-style investment strategies and structured notes.

Disclosure: Claro Advisors Inc. (“Claro”) is a Registered Investment Advisor with the U.S. Securities and Exchange Commision (“SEC”) based in the Commonwealth of Massachusetts. Registration of an Investment Advisor does not imply a specific level of skill or training. Information contained herein is for educational purposes only and is not considered to be investment advice. Claro provides individualized advice only after obtaining all necessary background information from a client.

The investment products discussed herein are considered complex investment products. Such products contain unique features, risks, terms, conditions, fees, charges, and expenses specific to each product. The overall performance of the product is dependent on the performance of an underlying or linked derivative financial instrument, formula, or strategy. Return of principal is not guaranteed and is subject to the credit risk of the issuer. Investments in complex products are subject to the risks of the underlying reference asset classes to which the product may be linked, which include, but are not limited to, market risk, liquidity risk, call risk, income risk, reinvestment risk, as well as other risks associated with foreign, developing, or emerging markets, such as currency, political, and economic risks. Depending upon the particular complex product, participation in any underlying asset (“underlier”) is subject to certain caps and restrictions. Any investment product with leverage associated may work for or against the investor. Market-Linked Products are subject to the credit risk of the issuer. Investors who sell complex products or Market-Linked Products prior to maturity are subject to the risk of loss of principal, as there may not be an active secondary market. You should not purchase a complex investment product until you have read the specific offering documentation and understand the specific investment terms, features, risks, fees, charges, and expenses of such investment.

The information contained herein does not constitute an offer to sell or a solicitation of an offer to buy securities. Investment products described herein may not be offered for sale in any state or jurisdiction in which such offer, solicitation, or sale would be unlawful or prohibited by the specific offering documentation.

©2025 by Claro Advisors, Inc. All rights reserved.

For all Market-Linked Products, excluding Market-Linked CDs, the following applies: Not FDIC insured // Not bank guaranteed // May lose value // Not a bank deposit // Not insured by any government agency